Bitcoin’s June Drop and the Michael Saylor Strategy Problem: A Technical Breakdown

TLDR

- Strategy Inc., formerly MicroStrategy, is no longer just a software company with Bitcoin on the balance sheet. It describes itself as the world’s first and largest Bitcoin treasury company.

- Its core machine is simple to describe but hard to sustain: issue common stock, preferred stock, convertible debt, or other securities; use the proceeds to buy or manage Bitcoin; and try to increase Bitcoin per common share over time.

- June 2026 tested that machine. Strategy disclosed a small sale of 32 BTC for about $2.5 million, maintained an 11.50% annual dividend rate on its STRC preferred stock, and moved STRC from monthly to semi-monthly dividends.

- The bull case is that Strategy built a public-market Bitcoin accumulation vehicle with access to capital markets, corporate-finance tools, and a clear per-share Bitcoin metric.

- The bear case is that the model depends on market confidence, a useful premium to Bitcoin net asset value, manageable financing costs, and investor appetite for preferred dividends and common-share issuance.

- MSTR, STRK, STRC, STRF, and STRD are not interchangeable. They sit in different parts of Strategy’s capital stack and have different upside, dividend, conversion, and seniority profiles.

- Hawaii readers should not confuse MSTR with direct Bitcoin ownership. A share of MSTR is a claim on a public company with debt, preferred stock, operating risk, dilution risk, tax risk, and Bitcoin price exposure.

This article is not personal financial, legal, tax, or investment advice. It is a technical explainer for residents who see Saylor, MSTR, and Bitcoin treasury content online and want to understand the structure before forming an opinion.

What Happened In June 2026

The June 2026 controversy around Strategy was not only about the price of Bitcoin. It was about trust in a financial structure.

Strategy had spent years building a public identity around Bitcoin accumulation. Michael Saylor, the company’s founder and executive chairman, became one of Bitcoin’s most visible corporate advocates. For many retail investors, “MicroStrategy” or “MSTR” became shorthand for a leveraged public-market Bitcoin bet.

Then the story became more complicated.

On June 1, 2026, Strategy filed an 8-K saying it had sold 32 BTC during the period from May 26 to May 31. The aggregate sale price was about $2.5 million, net of fees and expenses, at an average sale price of $77,135 per Bitcoin. The same filing said Strategy held 843,706 BTC as of May 31, 2026, acquired at an aggregate purchase price of $63.87 billion and an average purchase price of $75,699 per Bitcoin. The filing also said proceeds from the Bitcoin sales were expected to be used to fund distributions on preferred stock.

In ordinary corporate finance terms, that sale was tiny. Thirty-two Bitcoin was a rounding error next to more than 843,000 Bitcoin.

In narrative terms, it mattered. MarketWatch reported on June 1, 2026 that Strategy’s stock fell after the sale because it tested the company’s “never sell” image. The Wall Street Journal later described Saylor as saying Bitcoin’s slump reflected a rotation of capital toward AI rather than a fundamental rejection of Bitcoin. Investor’s Business Daily, writing on June 18 and June 19, focused on the pressure from preferred-stock financing costs, dividend obligations, and weaker buying power after Bitcoin and MSTR both fell.

So the technical question is not “Did Strategy dump its Bitcoin?” It did not, based on the numbers disclosed. The better question is:

What happens when a Bitcoin treasury company must support both its Bitcoin accumulation story and the securities it issued to finance that story?

Why Strategy Matters To Bitcoin Markets

Strategy matters because it made corporate Bitcoin accumulation investable through public securities.

An individual can buy Bitcoin directly, hold it in self-custody, keep it with an exchange, or buy a spot Bitcoin ETF. Strategy offers something different: exposure to a public company that holds a very large Bitcoin position and actively uses capital markets to grow or manage that position.

Strategy says its treasury strategy uses proceeds from equity and debt financings, plus operating cash flow, to strategically accumulate Bitcoin. Its investor-relations page describes the company as a Bitcoin treasury company that offers investors varying degrees of economic exposure to Bitcoin through equity and fixed-income instruments.

That matters for Bitcoin because Strategy is not a passive holder in the way a long-term individual wallet might be. It is a public issuer. It can sell common stock. It can issue preferred stock. It can issue convertible debt. It can repurchase debt. It can build cash reserves. It can use preferred-stock structures to attract income-oriented investors. It can also become a source of market anxiety if investors believe those obligations will force dilution, higher financing costs, or Bitcoin sales.

For Hawaii readers, the local angle is financial literacy. Residents may see clips that frame Saylor as either a Bitcoin hero or a reckless financial engineer. Neither frame is enough. If a Hawaii retail investor owns MSTR in a brokerage account, that person owns a security issued by a corporation, not a direct slice of Bitcoin sitting in a personal wallet.

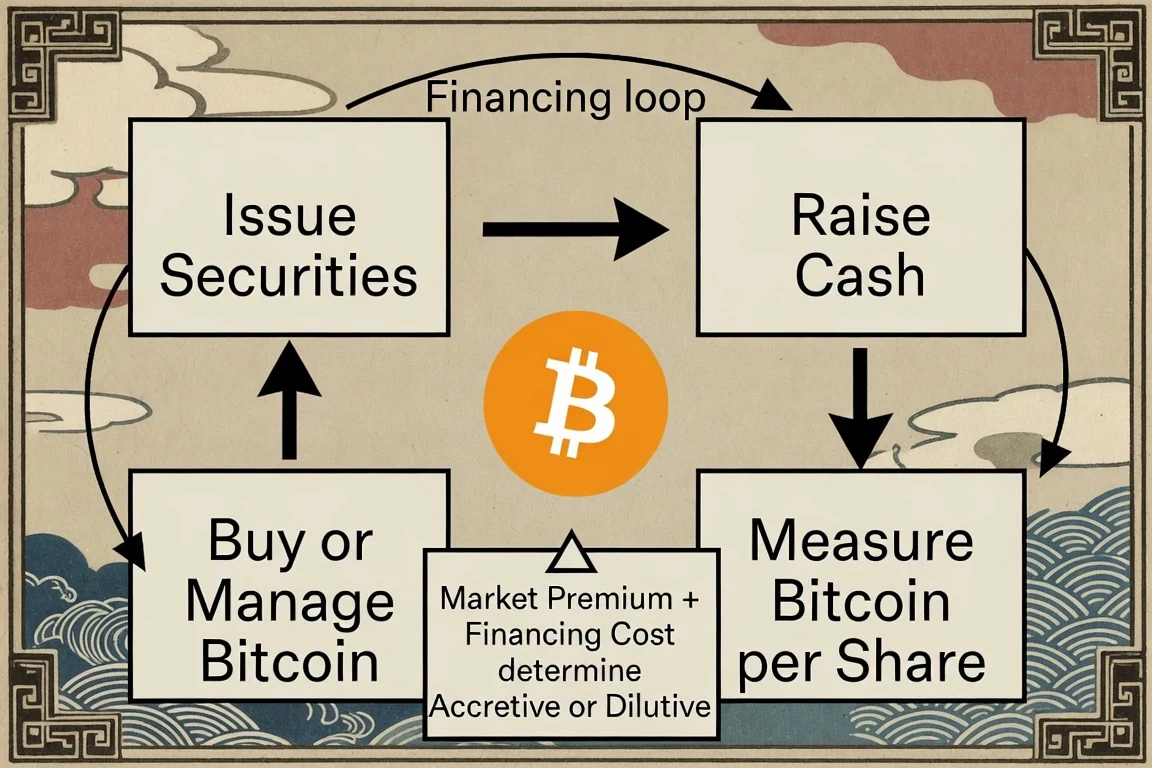

The Basic Machine

The Strategy model has four moving parts.

- Strategy holds Bitcoin as its primary treasury reserve asset.

- It raises capital through common stock, preferred stock, convertible notes, and other securities.

- It uses proceeds to buy Bitcoin, manage liabilities, or support obligations such as dividends and interest.

- It tracks whether those actions increase Bitcoin per share, especially for common shareholders.

The clean version looks like this:

Issue securities -> raise cash -> buy or manage Bitcoin -> try to improve Bitcoin per share -> repeat when conditions are favorable.

The hard part is that every financing source has a cost.

Common stock can dilute existing shareholders. Convertible notes can become shares later or require repayment/refinancing. Preferred stock can create dividend expectations or obligations ahead of common shareholders. Selling Bitcoin can solve a short-term cash need but weaken the accumulation narrative.

That is why Strategy’s model is not simply “buy Bitcoin.” It is closer to a corporate-finance engine built around Bitcoin as the main reserve asset.

Bitcoin Treasury Company

A Bitcoin treasury company is a public company that makes Bitcoin central to its balance sheet and capital allocation.

Traditional companies may hold cash, Treasury bills, short-term investments, inventory, receivables, property, and operating assets. A Bitcoin treasury company makes Bitcoin a primary reserve asset and then designs its financing strategy around that position.

Strategy still operates an enterprise analytics software business. But its market identity is dominated by Bitcoin. Its May 5, 2026 first-quarter press release described Strategy as the largest corporate holder of Bitcoin and the world’s first Bitcoin treasury company. It said the company held 818,334 BTC as of May 3, 2026. By May 25, 2026, Strategy said it held 843,738 BTC, had 220,900 Bitcoin per share in sats, had $6.7 billion of aggregate principal amount of convertible notes outstanding, $15.5 billion of aggregate notional amount of preferred stock outstanding, and a USD Reserve of $871 million.

Those numbers show why the company is technically interesting. Strategy is not only making a Bitcoin price bet. It is managing a layered capital structure around that bet.

BTC Per Share

BTC per share is the core metric behind the Strategy thesis.

Strategy defines Bitcoin Per Share, or BPS, as the ratio between its Bitcoin holdings and assumed diluted shares outstanding, expressed in satoshis. A satoshi is one one-hundred-millionth of a Bitcoin. Strategy uses BTC Yield to measure the percentage change in BPS over time.

The idea is straightforward:

- If Strategy raises capital in a way that lets it buy more Bitcoin per share than it gives up through dilution or future claims, BPS can rise.

- If Strategy issues shares or securities but does not add enough Bitcoin value for common shareholders, BPS can fall.

- If preferred stock or debt holders have senior claims, common shareholders may not receive the full economic benefit implied by headline Bitcoin holdings.

Strategy itself warns investors not to overread these metrics. In its May 5, 2026 release, the company said BPS does not represent its ability to satisfy obligations or book value per share, and that owning a share of common stock does not represent ownership of the Bitcoin held by the company. It also noted that the KPIs do not account for liabilities, preferred-stock rights, or claims senior to common equity in a liquidation.

That warning is important. BTC per share is useful, but it is not the same as owning Bitcoin.

NAV Premium And Discount

Net asset value, or NAV, is a way to estimate what Strategy’s assets are worth after considering liabilities and claims. In simplified conversations, people often compare Strategy’s market value to the value of its Bitcoin holdings.

When MSTR trades above the value of its underlying Bitcoin exposure, investors say it trades at a premium. When it trades below that reference value, investors say it trades at a discount.

The premium matters because common-share issuance is more attractive when the market values MSTR richly. If Strategy can sell shares at a premium and buy Bitcoin with the proceeds, the transaction may increase BTC per share. That is the ideal version of the flywheel.

The discount matters because the same issuance can become unattractive. If MSTR trades cheaply relative to the company’s Bitcoin and claims, selling common stock can dilute existing holders without adding enough Bitcoin per share. In that environment, preferred stock or debt may become more important, but those tools bring their own costs.

This is the tension behind June 2026. The model works best when investors want to fund the machine. It gets harder when the market asks the machine to prove it can fund itself.

Capital Stack At A Glance

The easiest way to understand Strategy is to separate the claims. The Bitcoin may sit on one corporate balance sheet, but not every security has the same place in line.

| Layer | What It Is | What Investors Want | Main Risk For Common Shareholders |

|---|---|---|---|

| Convertible notes | Debt that may be repaid, refinanced, repurchased, or converted under its terms | Principal protection, conversion upside, or favorable repurchase terms | Refinancing pressure, future share issuance, or cash use before common holders benefit |

| Preferred stock | Senior equity with stated dividend features and liquidation preferences | Dividend credibility, price stability, and priority over common stock | Cash drain, higher financing costs, and senior claims on assets |

| Class A common stock (MSTR) | The public equity most retail investors track | Leveraged upside if Bitcoin rises and BTC per share improves | Dilution, premium compression, and residual claim status behind debt and preferred stock |

| Bitcoin holdings | Treasury reserve asset held by Strategy | Balance-sheet appreciation and strategic optionality | Price volatility, tax/accounting effects, and possible sales to support obligations |

| Software business and cash reserve | Operating business plus liquidity used for dividends, interest, and flexibility | Ongoing cash flow and funding support | If insufficient, the company may rely more heavily on security issuance or Bitcoin sales |

This table is why headline Bitcoin holdings can be misleading. Common shareholders care about the residual value after liabilities, preferred-stock rights, future dilution, and operating needs are considered.

What The Strategy Tickers Mean

Strategy’s ticker list can be confusing because the names sound related but the securities are not the same product. As of June 2026, the main U.S.-listed tickers to understand are MSTR, STRC, STRK, STRF, and STRD. Strategy also has STRE listed on the Luxembourg Stock Exchange, but most Hawaii retail brokerage conversations will focus on the Nasdaq-listed securities.

The table below is a plain-English map, not a recommendation.

| Ticker | Security Type | Basic Mechanic | Potential Appeal | Main Tradeoff |

|---|---|---|---|---|

| MSTR | Class A common stock | Common equity in Strategy, the operating company and Bitcoin treasury company | Most direct public-equity upside if Bitcoin rises, MSTR’s premium expands, and BTC per share improves | Lowest place in the equity stack; can be diluted by new share issuance, conversions, and stock-paid dividends |

| STRC | Variable Rate Series A Perpetual Stretch Preferred Stock | Preferred stock with a variable regular dividend rate; Strategy said the rate was 11.50% in the March 23, 2026 annex and maintained 11.50% for June 2026 | Designed for investors who want preferred-stock income exposure rather than common-stock upside | Not convertible into common stock; dividend-rate changes and market confidence can move the price, and the company has discretion within the terms |

| STRK | 8.00% Series A Perpetual Strike Preferred Stock | Preferred stock with cumulative dividends and conversion rights into Class A common stock; declared dividends may be paid in cash, common stock, or both | Hybrid profile: preferred-stock income features plus possible common-stock conversion upside | More complex than ordinary preferred stock; stock-paid dividends or conversion can add common-share dilution |

| STRF | 10.00% Series A Perpetual Strife Preferred Stock | Preferred stock with cumulative cash dividends and no conversion rights | Higher-priority preferred claim than several other Strategy equity securities, with stated cash-dividend structure | Still junior to debt; cash dividends depend on legal availability and board declaration, and funding may require capital raising |

| STRD | 10.00% Series A Perpetual Stride Preferred Stock | Preferred stock with non-cumulative cash dividends if declared; no conversion rights | Simpler cash-income preferred structure than STRK or STRC | Non-cumulative means missed undeclared dividends do not accrue; it ranks junior to STRF, STRC, STRK, and debt |

For a beginner, the cleanest distinction is this: MSTR is the residual common-equity bet, STRK is the hybrid preferred with conversion features, STRC is the variable-rate preferred, STRF is a cumulative cash preferred with higher equity seniority, and STRD is a non-cumulative cash preferred that sits lower than the other preferred issues.

That matters because a social media post saying “Strategy stock” may refer to very different risk profiles. A common shareholder wants upside after everyone else is accounted for. A preferred holder may care more about stated dividends, payment priority, redemption terms, conversion features, and whether the market trusts Strategy’s ability to keep funding the capital stack.

Preferred Stock And Dividend Obligations

Preferred stock sits between debt and common equity in the capital stack. It usually has rights that common stock does not have, such as stated dividends or liquidation preferences, but it is still generally junior to debt.

Strategy’s preferred-stock lineup in June 2026 included STRF, STRC, STRK, STRD, and STRE. The June 1 8-K listed quarterly dividends for several preferred issues and a monthly STRC dividend of $0.958333333 per share for the month ending June 30, 2026, representing an 11.50% per annum dividend rate.

On June 8, 2026, Strategy announced that stockholders had approved moving STRC from monthly to semi-monthly dividend record dates and payment dates. On June 15, 2026, the company filed an 8-K saying the amendment would become effective on June 30 and would provide for two scheduled dividend payment dates per month instead of one. The filing said the modification did not change STRC’s dividend rate or increase overall dividend payment obligations, but it changed timing and cadence.

From the bull side, this is financial engineering designed to attract investors who want income and liquidity. From the bear side, it adds another confidence test. If preferred investors demand higher yields, if STRC trades below par, or if dividend credibility weakens, the financing engine becomes more expensive.

Investor’s Business Daily reported on June 18, 2026 that STRC’s annual dividend rate had risen from 9% at launch to 11.5% and could move higher if its price stayed below threshold levels. That is a market-reaction source, not a guarantee of future board action. But it captures the risk: preferred-stock financing can look elegant when demand is strong and punishing when demand weakens.

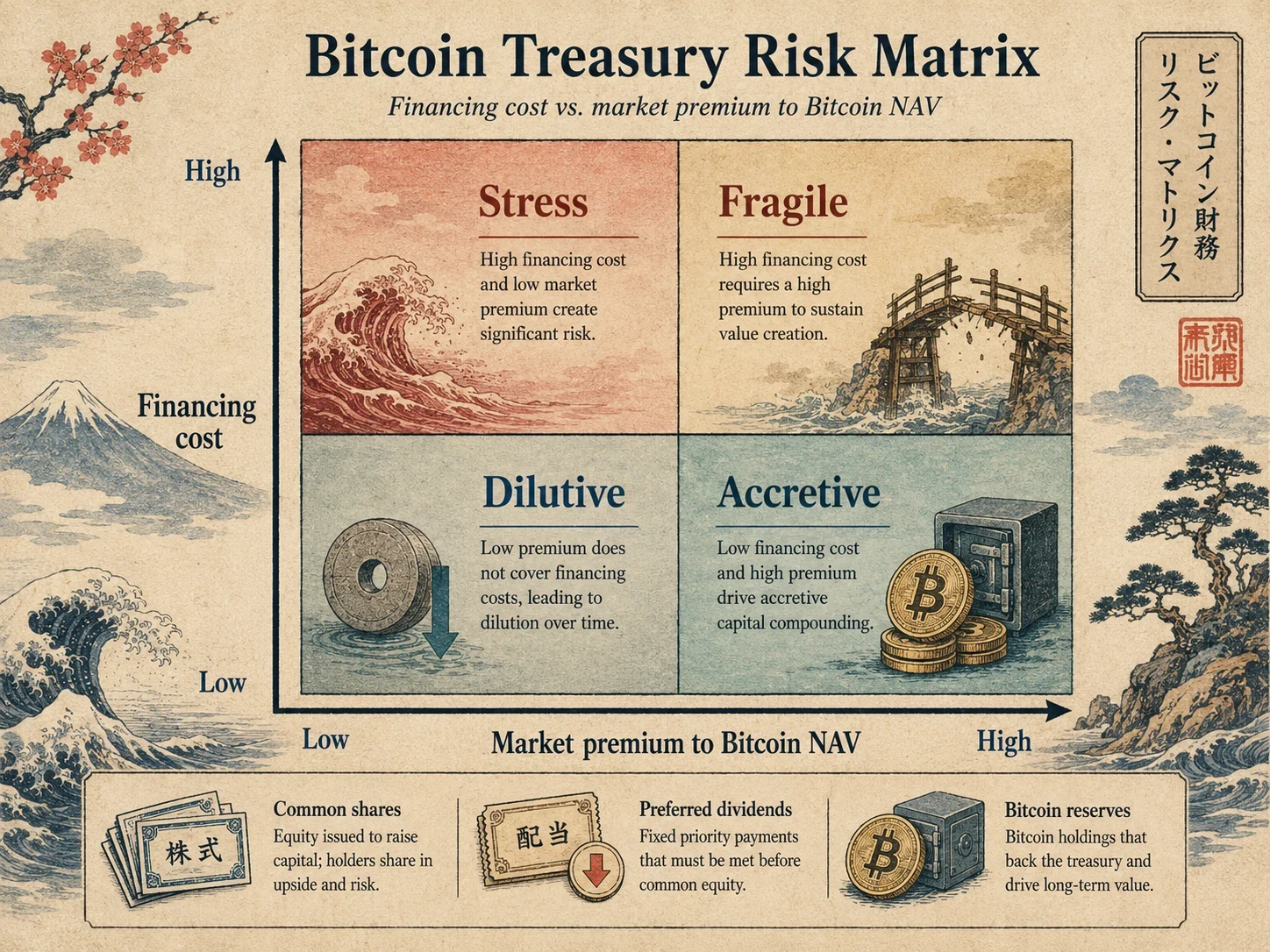

Accretion Versus Dilution

Accretion means a financing action improves the per-share economics for common shareholders. Dilution means it worsens them.

For a Bitcoin treasury company, the question is not only “Did the company buy more Bitcoin?” The better question is:

Did the company buy enough Bitcoin, on good enough terms, to improve the claim of each common share after considering new shares, debt, preferred stock, dividends, and senior claims?

A simple example:

- If a company has 100 BTC and 100 shares, it has 1 BTC per share before liabilities.

- If it sells 10 new shares at a high premium and uses the cash to buy 20 BTC, it now has 120 BTC and 110 shares, or about 1.09 BTC per share before liabilities. That is accretive.

- If it sells 50 new shares and only buys 20 BTC, it now has 120 BTC and 150 shares, or 0.80 BTC per share before liabilities. That is dilutive.

Real Strategy math is more complex because of convertible securities, preferred stock, operating assets, taxes, and financing costs. But the intuition is the same.

The Bull Case, Steelmanned

The strongest argument for Strategy is that it created a new type of public-market Bitcoin accumulation vehicle.

First, Strategy has scale. As of May 31, 2026, the company disclosed 843,706 BTC. That is not a casual treasury allocation. It is a corporate identity.

Second, it has capital-markets access. Many Bitcoin holders can only buy with cash they already have. Strategy can raise capital through common stock, preferred stock, convertible notes, and other instruments. When markets are receptive, that flexibility can let the company accumulate Bitcoin faster than a passive holder.

Third, Strategy has created a clear performance language around BTC per share. Investors can debate the metric, but the goal is transparent: grow the Bitcoin exposure behind each common share over time.

Fourth, preferred stock can broaden the investor base. Some investors do not want volatile common equity but may want income-oriented securities connected to a Bitcoin-heavy company. Strategy’s preferred products are designed to separate different risk appetites into different securities.

Fifth, the company has shown it can use liability management. On May 26, 2026, Strategy announced it had completed a $1.5 billion aggregate principal amount repurchase of 0% convertible senior notes due 2029 for about $1.38 billion in cash, an approximate 8% discount to par. It framed the transaction as part of a dynamic capital allocation model.

In the bull version, Strategy is not merely leveraged Bitcoin. It is a specialized financial company using volatility, investor demand, and security design to acquire and manage Bitcoin in ways a spot ETF cannot.

The Bear Case, Steelmanned

The strongest argument against Strategy is that the structure depends on confidence.

The model needs investors to keep valuing MSTR and Strategy’s preferred securities in ways that let the company raise capital on favorable terms. If that appetite fades, the flywheel slows.

The model also depends on financing costs staying manageable. Preferred dividends are not the same as bank debt, but they are still a recurring cash expectation. If investors demand higher yields, preferred financing becomes more expensive. If Strategy uses common stock when the share price is weak, common holders may face dilution. If it sells Bitcoin to fund obligations, the sale may be financially small but symbolically large.

The bear case also focuses on senior claims. Common shareholders sit behind debt and preferred stock. Strategy’s own KPI language acknowledges that its Bitcoin is subject to liabilities and preferred-stock rights. That means common shareholders cannot simply divide total Bitcoin by share count and assume they own that amount free and clear.

Finally, the model may become more fragile during Bitcoin drawdowns. Lower Bitcoin prices can reduce the value of collateral-like assets, weaken investor enthusiasm, pressure MSTR’s premium, and make income securities demand higher yields. Those effects can reinforce each other.

The bear case does not require believing Strategy is insolvent or that a forced Bitcoin sale is inevitable. It only requires believing the company’s capital structure becomes less forgiving when Bitcoin falls and the market premium narrows.

Why The Small Bitcoin Sale Mattered

The June 1 sale mattered because it changed the story from “Strategy never sells Bitcoin” to “Strategy may sell Bitcoin selectively to support the broader capital structure.”

Again, the numbers were small: 32 BTC sold, compared with 843,706 BTC held after the sale. The filing said proceeds were expected to fund preferred-stock distributions. That is not evidence of a massive liquidation.

But symbols matter in finance. If a public company builds confidence around a one-way accumulation narrative, even a tiny sale can force investors to ask what the real hierarchy is:

- Is the highest priority never selling Bitcoin?

- Is the highest priority increasing BTC per share?

- Is the highest priority protecting preferred-stock credibility?

- Is the highest priority maintaining access to capital markets?

The practical answer may be “all of the above, depending on conditions.” That is exactly why the structure deserves technical analysis instead of slogans.

Direct Bitcoin Versus MSTR Exposure

Direct Bitcoin and MSTR are different instruments.

Direct Bitcoin exposure means the investor owns Bitcoin or a claim designed to track Bitcoin directly, such as a spot ETF. The risks include price volatility, custody, fees, taxation, exchange risk, and regulatory changes.

MSTR exposure means the investor owns common equity in Strategy. That adds Bitcoin price exposure, but also adds corporate-finance risk:

- Common-share dilution

- Preferred-stock dividends and liquidation preferences

- Convertible-note refinancing or conversion

- Operating business performance

- Tax accounting and deferred tax effects

- Market premium or discount to Bitcoin NAV

- Governance and management execution

- Narrative risk around Saylor and the company’s public commitments

That does not make MSTR automatically better or worse. It makes it different.

A Hawaii resident comparing direct Bitcoin, a Bitcoin ETF, and MSTR should understand the instrument before comparing returns. MSTR can outperform Bitcoin in some conditions because of leverage, premium expansion, and capital-markets execution. It can underperform Bitcoin when dilution, financing costs, discount pressure, or confidence problems dominate.

What Hawaii Readers Should Learn

Hawaii has a unique crypto history. Residents remember years when major exchanges avoided the state because of regulatory uncertainty. Hawaii’s Digital Currency Innovation Lab ended on June 30, 2024, and local access to crypto services has changed significantly since then. At the same time, residents still face the usual risks of national crypto marketing, social media narratives, and financial products that are easy to misunderstand.

Strategy is a useful case study because it sits between Bitcoin culture and Wall Street structure.

The lesson is not “buy MSTR” or “avoid MSTR.” The lesson is to identify what you actually own.

If you own Bitcoin in self-custody, you are managing private-key and market-price risk. If you own a spot Bitcoin ETF, you are accepting fund structure, fees, custody arrangements, and market tracking. If you own MSTR, you are buying a public company’s common stock with a complex capital stack tied to Bitcoin.

That distinction matters for local investors, small-business owners, and families who may discuss Bitcoin as if every exposure is the same. It is not the same.

Practical Risk Checklist

Before treating MSTR as “Bitcoin in a brokerage account,” ask:

- Does MSTR trade at a premium or discount to the value of Strategy’s Bitcoin holdings after considering liabilities and preferred claims?

- Is the company issuing common stock, preferred stock, convertible debt, or selling Bitcoin?

- Are new financings likely to increase or decrease BTC per common share?

- What dividend rates and payment obligations exist on preferred stock?

- How much cash reserve does the company disclose for dividends and interest?

- What happens if Bitcoin falls and capital markets become less receptive at the same time?

- Are you reading company filings, or only social media summaries?

- Are you comfortable owning a company security instead of direct Bitcoin?

- Are you prepared for MSTR to move differently from Bitcoin, including amplified gains or losses?

For Hawaii readers, add one more question: would you still understand the position if the social-media personality disappeared from the explanation? If the answer is no, the product may be too narrative-driven for your current risk process.

Conclusion

Strategy’s Bitcoin treasury model is innovative, but it is not simple.

The bull case deserves respect. Strategy created a large public-market Bitcoin vehicle, used capital markets aggressively, and built a framework around Bitcoin per share. It gave investors securities with different exposure profiles and showed that a public company can make Bitcoin the center of its capital strategy.

The bear case also deserves respect. The model depends on market appetite, share premium, preferred-stock credibility, financing costs, liquidity, and continued confidence in management’s capital allocation. June 2026 exposed that fragility because a small Bitcoin sale became a large narrative event.

The best way to understand Strategy is not as a hero story or a collapse story. It is a live corporate-finance experiment built on Bitcoin. That makes it important, fascinating, and risky in ways direct Bitcoin ownership is not.

Sources

- Strategy investor relations page, accessed June 19, 2026.

- Strategy press release, “Strategy Announces First Quarter 2026 Financial Results,” May 5, 2026.

- Strategy press release, “Strategy Completes $1.5 Billion Debt Repurchase and achieves BTC Yield of 13.3% YTD; Now Holds 843,738 BTC,” May 26, 2026.

- Strategy Form 8-K filed June 1, 2026.

- Strategy press release, “Strategy Announces Approval of STRC Semi-Monthly Dividends,” June 8, 2026.

- Strategy Form 8-K filed June 15, 2026.

- Strategy Common Stock ATM Annex, March 23, 2026.

- Strategy STRC ATM Annex, March 23, 2026.

- Strategy STRK ATM Annex, March 23, 2026.

- Strategy STRF ATM Annex, November 4, 2025.

- Strategy STRD ATM Annex, November 4, 2025.

- MarketWatch, “Strategy’s stock drops after rare bitcoin sale tests ‘never sell’ narrative,” June 1, 2026.

- Wall Street Journal, “Bitcoin Slump Is a ‘Capital Rotation’ to AI, Strategy’s Michael Saylor Says,” June 4, 2026.

- Investor’s Business Daily, “Bitcoin Whale Faces Gut Punch: Borrowing Rate May Hit 12%,” June 18, 2026.

- Investor’s Business Daily, “Bitcoin Whale Pays Price For Borrowing Binge As Buying Power Flags,” June 19, 2026.